Put Down Your Shovels

Happy Monday Morning!

After holding rates last week, Tiff Macklem was summoned to parliament for more berating by concerned politcians wondering when the beatings will end. In regards to rate cuts, “We can’t put it on the calendar,” Macklem said. “We need to see how inflation evolves.”

CPI inflation is still running at 3.4%, well above the banks target, but when you strip out shelter costs we are resting comfortably at 2.4%. There’s just one problem, shelter is a neccessity, something you can’t go without, and shelter inflation remains incredibly sticky.

Typically “as interest rates go up, you would see a decline in house prices,” senior deputy governor Carolyn Rogers told the parliamentary committee. “But because we have sort of a chronic, structural shortage of housing in Canada, we haven’t seen that sort of offset.”

It’s true, price declines in most major markets have been modest. The collateral damage from a highly levered housing market colliding with the most aggressive tightening cycle in recent history has largely been contained to a few frothy suburbs. Consider me as surprised as Mrs. Rogers.

However, population growth is running at 70 year highs, something that wasn’t accounted for in any forecasts and certainly not in any economic models.

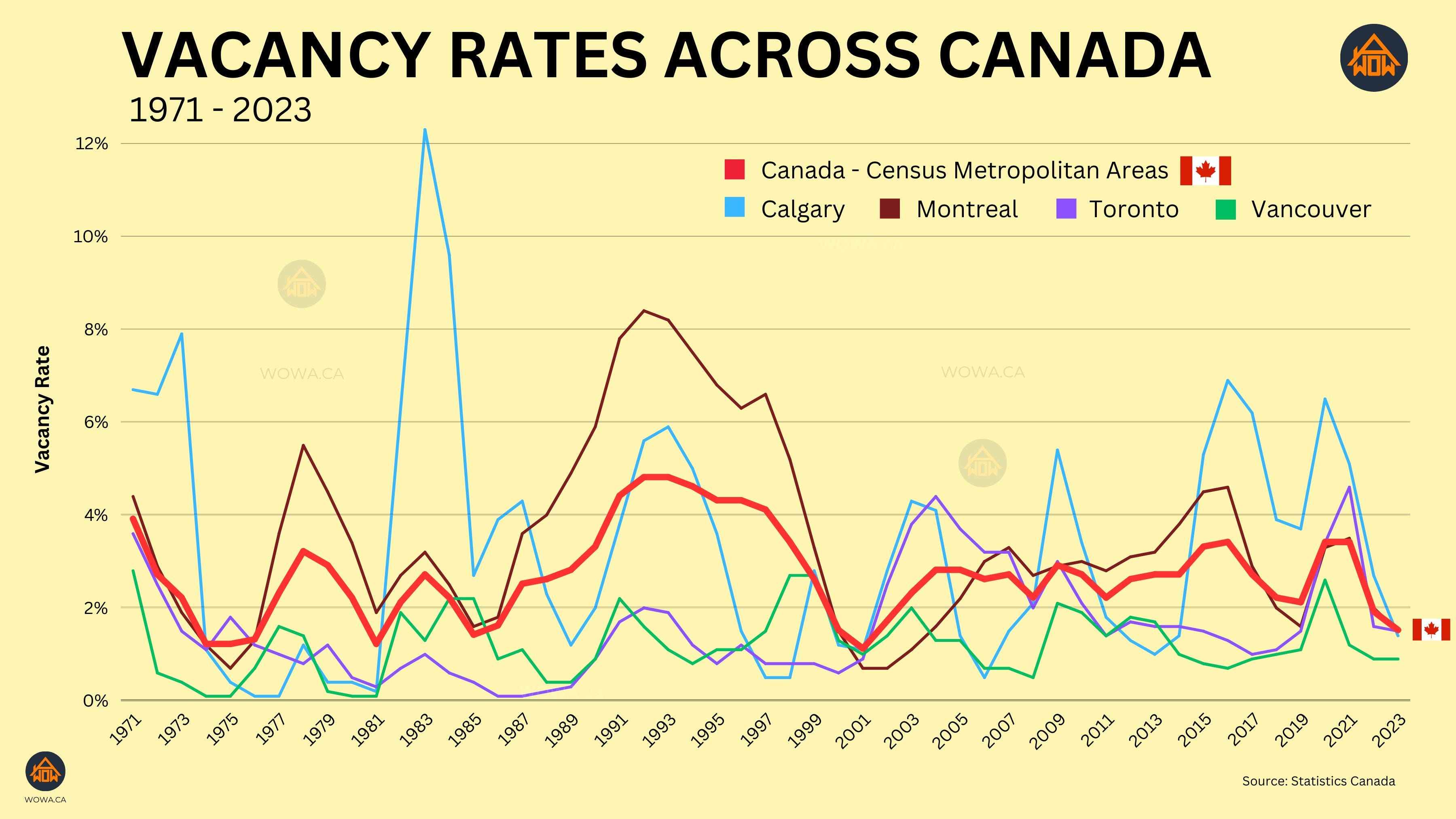

Not ony has this cushioned home prices but it’s set the rental market on fire. According to a recent report from CMHC, the vacancy rate in Canada slipped to 1.5% as recently as October. That’s the lowest vacancy rate in the past 38 years (outside of 2001).

Annual rent inflation is currently humming at 8%, while turnover rents surged to 24% year-over-year. People are doing what they need to in order to survive, including sharing a basement with 25 other students.

So long as this continues, it’s reasonable to think shelter inflation could remain elevated, prompting the BoC to push rate cuts further down the line, particularly if the resale market holds up.

This would be rather ironic considering the fact that higher interest rates are actually choking off new supply, rendering most projects economically unviable. To which Tiff is well aware.

“Yes, there is an impact on the supply side,” he told members of Parliament. “Developers have pointed that out. But when we look at the sector as a whole, the impact on demand is much stronger than on the supply side.”

Perhaps.

According to Urbanation, new condo sales in the GTA fell 41% in 2023 to a 15-Year Low.

Developers are now sitting on a pile of unsold inventory. Unsold new condo inventory increased 41% year-over-year to 22,477 units in Q4-2023. In other words put down your shovels, immediately.

Per Urbanation, construction activity in the GTA fell considerably in the second half of 2023, recording only 4,397 starts — a 72% plunge from the same period in 2022.

In other words, high rates, low rates, we are seemingly pooched either way.

I don’t have the data for BC, but we are trending in the same direction. Housing starts will fall like a sack of potatoes this year.

In other news, the federal government extended the two year ban on foreign buyers. The current ban on foreign ownership was set to expire next year, and will now remain in place until January 2027.

The ban is littered with loopholes, and much like the foreign buyers tax which was introduced in 2016, it will fail to deliver on the only measuring stick that matters, affordability.

Inflation is the imposition of liabilities —prices — on us by those with the power to impose prices. The purpose is to extract or transfer more assets for the benefit of those with the power to set prices. Mythical supply and demand curves do not actually apply but demand-pull explanations are preferred to cost-push ones as the cover story.

When central banks raise interest rates to allegedly fight inflation they signal the financial markets to impose more liabilities in order to transfer more assets to those financial operatives.

Purely and simply, inflation is price gouging by those with the power to do so when there are or may be some shortages in supplies. They may not be real but expectations of shortages also justifies raising prices and imposing liabilities just in case shortages occur. Demand usually remains the same but the pretense is that it must be suppressed. That covers the real issue which is the facilitation of more transfers of assets to those with power to set prices.

In conclusion, inflation is yet another cover story for asset transfers to the wealthy as is raising interest rates to fight inflation. By focusing on price increases or liabilities, emotions are aroused stirring up more animal spirits to justify austerity measures.

The outcome of more liabilities and more asset transfers is more wealth and income inequality.