Happy Monday Morning!

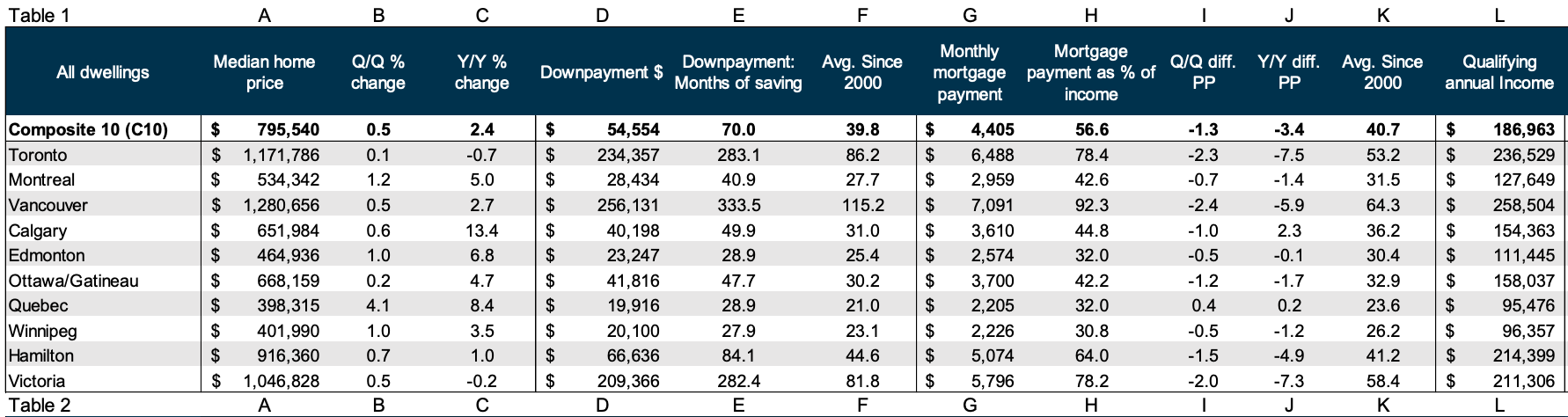

A good reminder from the economics team at National Bank highlights the sobering proposition that a Canadian household would need an annual income of approximately $186,963 to afford a mortgage on a median-priced home in this country, at which point the government thinks you're rich and taxes you into oblivion.

In places like Toronto and Vancouver the qualifying annual income jumps to $236,529 and $258,504 respectively. Not only does this mean you have to be in the top 5% of income earners just to service the mortgage, but it would also take you 23 years to save for a downpayment in Toronto, and 27 years in Vancouver.

I can tell you from firsthand experience working with home buyers on a regular basis that the biggest barrier to accessing the housing ladder is saving for the downpayment which is incredibly hard to do when you’re paying sky high rents and taxes. This is why parents, who are already on the housing ladder, are gifting large sums of cash to their kids. Call it a front on the inheritance.

It’s also why housing and the social contract are systemically broken in this country. The Feds are trying to lower the barrier to housing by lowering down payment requirements and increase tax payer subsidized loans on purchases up to $1.5M, but all this does is juice demand and supersize leverage.

We need to start thinking differently. How can we increase incomes and more importantly increase real after tax takehome pay? Because as it stands right now, Canada has seen the worst deterioration in after-tax income relative to house prices in the world.

Lowering income taxes seems like the obvious solution, but don’t hold your breath. House prices and taxes are inflating at a rate far exceeding incomes and we need to reverse course immediately.

The public sector is essentially cannibalizing the economy. From 2019 to 2023, public sector employment increased by 13.3%, compared to just 3.6% in the private sector (including self-employment). As of September 2024, public sector employees totaled 4.4 million, representing 21% of the total workforce. It costs tax payer dollars to keep feeding the machine, and many of those dollars are being derived from the housing sector.

Remember, about 30% of the cost of new housing today is just government fees and taxes. That which is unsustainable can not continue. For example, Toronto's development charges on a 2-bedroom apartment unit have risen by an average of over 17% a year for a decade. At this rate DCs will exceed $4 million by the end of Toronto's planning horizon (2051).

If you want to improve housing affordability over time you have to reduce taxes not just on the development side, but on the personal income side as well. Because, as we highlighted at the beginning of this note, $186,963 doesn’t buy you what it used to.

You (and your compatriots from the Loonie Hour) have the benefit of seeing these issues beyond single-sector effects - it's all intertwined. It would be great if, just as you indicated the problem with going our current course, you also critiqued your own recommendation of reducing taxes. Obviously that's A solution, but you didn't talk about the effects of doing so; I don't think anyone believes that lowering taxes will take us right back to Canada's heydays.. maybe having lower taxes is an important aspect of our 'steady state' economy, but how do we get there? If we lowered all of the taxes as you said, what would be the effect of that hole in govt budgets? Do you believe it's all just excess and waste and we could just carry on more efficiently but with the same services? Or will health spending get cut... education? social programs for seniors?

We can all be like the opposition and yell out simple solutions to the govt, but if you're in the know, wouldn't it be more effective to suggest a more comprehensive plan? Just like healthcare needs more money - what budget item will we pull it from? It's not like we're running surpluses that we can just dip into.

Sobering words, Steve. The problem has been central banks keeping the prime rate well below the intrinsic cost of capital over the past twenty years. This has led to massive asset appreciation which is now reflected in unaffordable housing. The current development charges, as you point out, are a result of the government sector feeding on the same trough.

The tragedy is that now Mr. Carney, the past president of our central bank, who was responsible for this disastrous monetary policy, is running to become our next leader. Sadly, the public cannot see the truth, as so many of the elite were feeding off Mr. Carney’s asset inflating policy.