Close The Gates

Happy Monday Morning!

A softer than expected US CPI print for the month of October. Consumer prices were up 7.7% year-over-year, and while still elevated they are decelerating. It was the biggest downside miss on the core CPI since Apr 2020. Long ways to go still but we have progress. Yields tumbled on the news, with the all important Canada 5 Year bond yield plummeting around 30bps.

Have we seen the peak in mortgage rates for this cycle? Probably. Interest rates are doing their job, crushing demand, destroying wealth, and bringing the economy and inflation down with it. Everywhere you look something is blowing up, no need to cover the FTX story, we’ll stick to Real Estate here as there’s plenty to talk about.

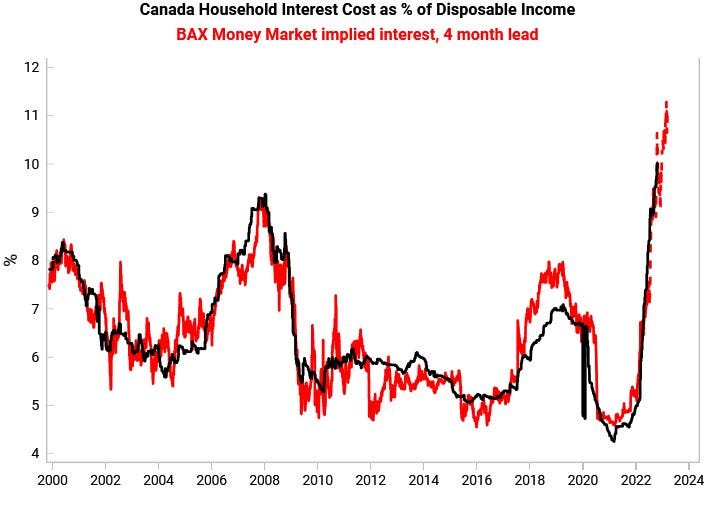

I went to one of the big banks last week to discuss converting a variable rate mortgage into a two year fixed rate mortgage. The best they could offer was a rate of 6.2%. I took a hard pass but many households coming up for renewal won’t have a choice. This is a huge interest rate shock for households. Household interest costs as a percentage of disposable income is now at its highest levels in more than two decades.

At RBC, the country’s largest mortgage lender with about 310,000 variable-rate mortgages, roughly 125,000 mortgage clients have reached or are nearing a trigger point that requires an immediate increase in monthly payments, according to Leah Robinson, vice-president of home equity financing policy and regulatory management.

Meanwhile, over at CIBC about $7-billion of variable-rate mortgages are up for renewal in the next 12 months, per The Globe & Mail.

More disposable income servicing mortgages, means a lot fewer Disney Plus subscriptions. Remember, one persons spending is another persons income.

In what is perhaps just another sign post, Romspen, one of Canada’s largest private mortgage lenders with more than $3.2B in assets, has frozen investor redemptions, citing ‘suppressed’ loan repayments. Per Romspen, “When rates changed quickly over the past few months it created an air pocket as many pending transactions were delayed or disrupted,” he wrote. “Ultimately, this affects short term cash flows and distributions as many deals that were being refinanced or sold around that time got delayed.”

In other words, these short term loans aren’t rolling over. Liquidity has dried up, and existing loans aren’t being paid back quick enough due to worsening conditions in the housing market.

Romspen has been around for more than thirty years, they are no dummies. If they are gating investor funds it’s only a matter of time until others follow suit. As highlighted by my friend Ron Butler, an increasing number of Mortgage Investment Corps are taking action via court ordered sales in order to get mortgages redeemed and get capital back to investors as redemption requests increase. The only problem is court-ordered sales take a long time in Canada, up to a year in most cases.

Suffice to say there are a lot of issues brewing beneath the surface in this nations financially systemic housing market. If you’re looking at the CPI index to tell you if inflation is coming down i’m afraid you’ll miss it.

However, if you want to know what’s already happened, October CPI and national housing data will be published later this week.