Banking on Rate Cuts

Happy Monday morning!

There a lot of Canadians holding their breath for rate cuts this year. Nearly 60% of Canadian mortgage holders haven’t endured a mortgage payment increase yet, but its coming. It’s a race against time to get inflation, bond yields, and the Bank of Canada’s overnight rate lower.

There’s just one problem, the last mile on getting inflation back towards 2% has proven challenging, and economic data really hasn’t deteriorated enough to warrant rate cuts. This is particularly the case for our neighbours to south which heavily influence our financial markets.

Did we jump the gun on rate cuts?

Market commentator Jim Bianco, who has been spot on regarding inflation for the past few years, highlighted some interesting observations recently. Per the February Bank of America Global Fund Managers Survey released last week, 90% expect the central bank to cut rates and 77% expect inflation to fall. The consensus is effectively a unanimous opinion.

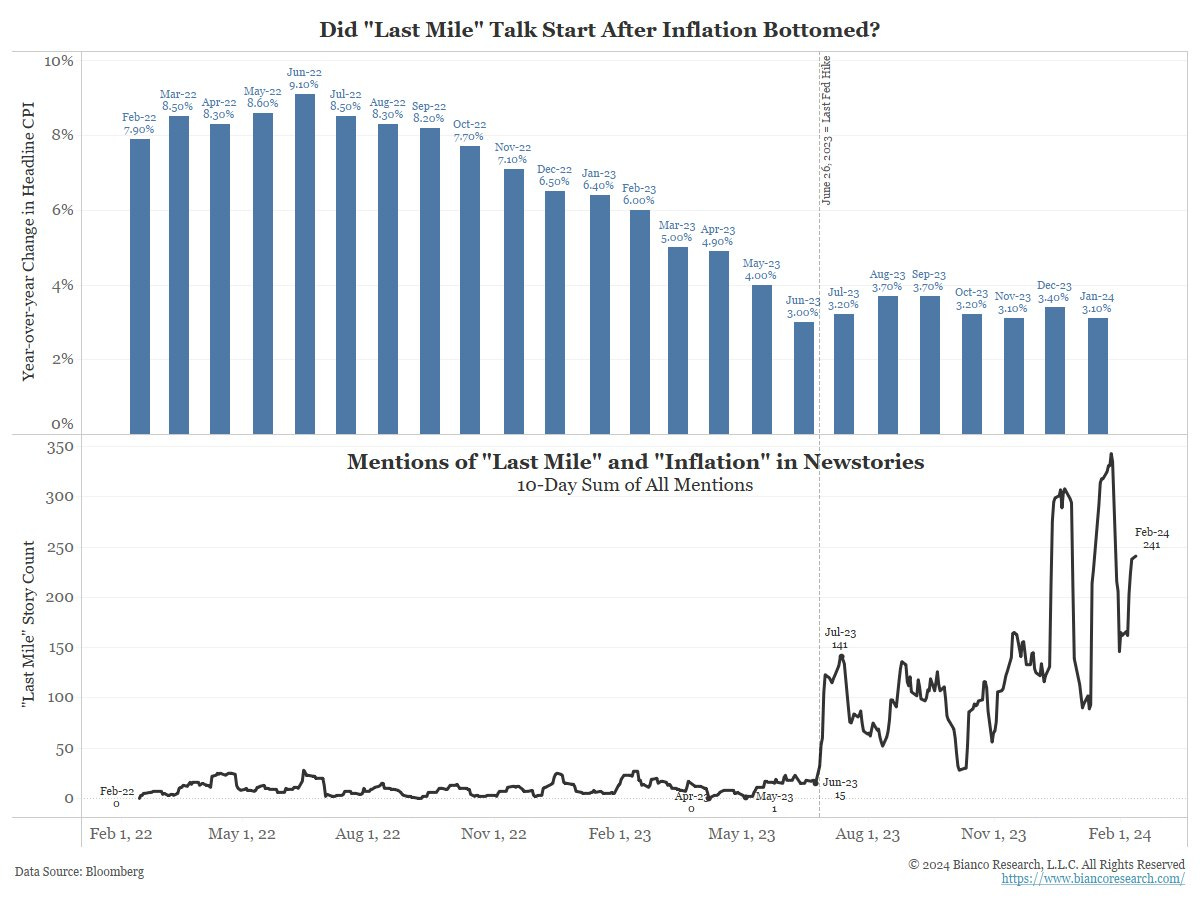

This strong consensus has created a narrative about a "last mile." The blue bars in the chart below show year-over-year headline CPI. Note that inflation peaked in June 2022 at 9.1%. Also note that year-over-year headline CPI bottomed at 3.0% in June 2023, seven months ago. The black line in the bottom panel shows a rolling 10-day sum of all news stories that contain the words “last mile” and “inflation.”

The last mile refers to the move from the current level of inflation (around 3%) to 2%. The “Last mile” began being used in June 2023 when inflation hit 3.0% and the Fed stopped hiking. However, in the seven months since this became the inflation narrative, inflation has stayed above its June 2023 low of 3.0%.

This is not the news markets were hoping for, and its certainly not the news Canadians were hoping for, including our housing minister.

“My expectation is if we see a dip in interest rates over the course of this year, a lot of the developers that I’ve spoken to will start those projects that are marginal today,” noted housing minister Sean Fraser.

Are we sure about that? If so, how much of a dip in interest rates will developers need to see to get off the sidelines?

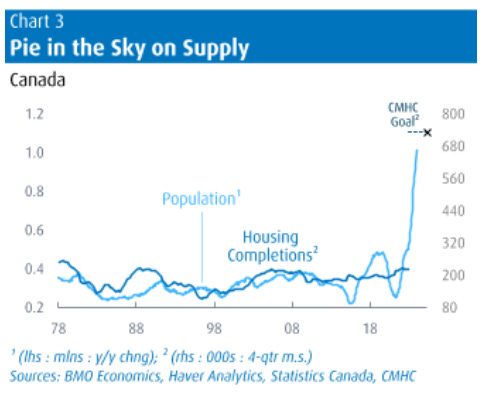

Building permits, which lead housing starts, are plunging. In the single family sector, which is the most nimble segment and able to pivot on a dime, has seen permit activity collapse. In BC & Ontario, single family housing permits have collapsed to their lowest levels in 40 years!

This trend is leaking into apartment permits as more projects fail to launch with insolvencies beginning to stack up.

It’s no wonder the team at BMO Economics suggested this week that Canada's housing targets were a pie in the sky. It does not matter how much you rezone, in the near term new housing starts are heading to the chopping block.

The unfortunate reality for Sean Fraser and his colleagues is that the economy needs to get worse before we get any meaningful rate cuts and a renewed uptick in housing starts.

Since the calendar turned over into the new year, the all important Canada 5 year bond yield has jumped 45bps, and markets went from expecting 5 rate cuts from the Bank of Canada to just 3. If that’s the case, that would leave variable rate mortgages stuck in the high 5’s for all of this year.

This is not what the housing minister, developers, or the millions of Canadians renewing their mortgage wanted to hear, but sometimes the truth hurts.

Perhaps the development project bankruptcies will be a good thing from a supply point of view? Allowing projects (if not their original investors) to get out from under unsustainable sunk costs from a previous market era?

Noticed many noncommittal buyers - started searching but needed the spring rate cut. RIP!